Tencent’s AI Aspirations

As AI sparks a new technological revolution, has Tencent secured its ticket to the next era? At the 2026 shareholder meeting, Tencent’s Chairman and CEO, Ma Huateng, remarked, “A year ago, we thought we were on board, only to find the ship was leaking. We quickly switched to another ship, and now we feel we are on it, but we still hope it can speed up.”

Clearly, Ma Huateng believes that after a year of arduous exploration, Tencent has boarded the ship heading towards the next era. According to financial reports, AI has indeed become a significant engine driving Tencent’s growth. In Q1 2026, with AI’s assistance, Tencent’s marketing services and enterprise services revenue grew by 20% year-on-year, far exceeding the overall revenue growth of 9%.

However, it’s important to note that Tencent is not an ordinary internet company; its business moat is primarily built on the relationship chains established by social products like WeChat and QQ, along with the resulting network effects.

In the PC era, Tencent leveraged QQ to easily venture into gaming, entertainment, and portal businesses. When smartphones emerged, WeChat seamlessly inherited QQ’s social relationship chain, helping Tencent secure its ticket to the mobile internet. Today, WeChat has not yet completed a true AI transformation, indicating that Tencent still faces significant uncertainties in the AI era.

Two Attempts at Boarding the Same Ship

As is well known, AI became the focus of the tech industry at the end of 2022 with the advent of ChatGPT. However, due to a greater emphasis on AI application implementation and the immaturity of model capabilities, Tencent did not aggressively pursue consumer-facing AI applications like ByteDance and Baidu.

It wasn’t until early 2025, when DeepSeek open-sourced DeepSeek-R1, providing a mature foundational model for latecomers, that Tencent began to fully ramp up its consumer AI assistant product, Yuanbao.

In mid-February 2025, Yuanbao integrated the full version of DeepSeek-R1, supporting online searches and integrating information sources from WeChat official accounts and video accounts. At the same time, Tencent began actively acquiring computing power, with capital expenditures in Q2 2025 reaching 19.1 billion yuan, a staggering 119% year-on-year increase.

To promote Yuanbao in the market, Tencent invested heavily in marketing. According to AppGrowing, Yuanbao’s total advertising spend in the first half of 2025 was approximately 6 billion yuan. As a result, Yuanbao briefly topped the free app charts in the China App Store.

Unfortunately, due to its positioning as merely a chatbot and lacking sufficient differentiation, Yuanbao inevitably faced user attrition in the second half of 2025 as Tencent’s marketing efforts waned.

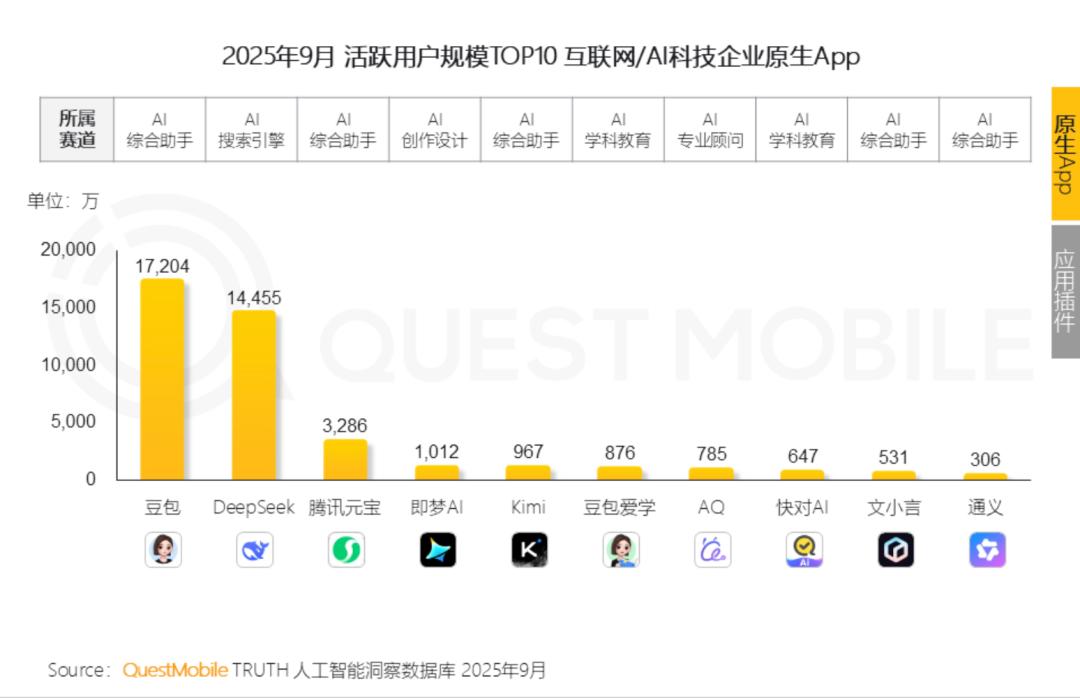

Data from QuestMobile revealed that Yuanbao’s monthly active users dropped from 42 million in March 2025 to 32.86 million in September, a decline of 21.76%. This led Ma Huateng to describe Yuanbao from a year ago as “leaking.”

However, Tencent did not abandon Yuanbao; instead, during the 2026 Spring Festival, it reignited a “marketing war” by launching a 1 billion yuan cash red envelope campaign. Ma Huateng stated, “We converted some of the huge marketing expenses spent by competitors on TV into red envelopes, hoping to recreate the moment of WeChat red envelopes during the Spring Festival 11 years ago.”

To enhance user engagement, Yuanbao leveraged Tencent’s social advantages by creating an AI social feature called “Yuanbao Group.” Users can create or join “group” chats in Yuanbao, where the embedded Yuanbao AI interacts with users based on chat content.

The Spring Festival red envelope campaign indeed injected massive traffic into the internet product. On February 18, 2026, Tencent announced that following the conclusion of the 1 billion yuan campaign, Yuanbao’s daily active users exceeded 50 million, with monthly active users reaching 114 million.

However, Yuanbao did not become a “evergreen tree” like WeChat red envelopes; after the Spring Festival traffic peak, its user base again plummeted. During the Q4 2025 and annual earnings call on March 18, 2026, Tencent’s President, Liu Chiping, revealed that Yuanbao’s daily active users had dropped to 18 million, a 64% decline from the Spring Festival period.

In summary, despite differing feature focuses in early 2025 and early 2026, and Tencent employing entirely different marketing strategies, the product still followed the same “leaking” script.

The reason lies in the fact that, despite gaining visibility through heavy marketing, Yuanbao has failed to cultivate differentiated competitive strength due to the lack of a strong self-developed foundational model.

According to LatePost, due to the inability to train DeepSeek specifically, and the relatively weak capabilities of Tencent’s mixed model, the Yuanbao team has been unable to validate certain ideas in the product, with many desired features remaining unimplemented. To this day, Yuanbao’s core functionality remains natural language dialogue, without establishing unique capabilities that distinguish it from products like Doubao, DeepSeek, and Kimi.

In contrast, Doubao has not driven its growth through heavy marketing like Yuanbao; instead, it focuses on the product, continuously aligning with user needs and launching new features.

For example, as early as 2023, Doubao launched real-time voice calling features, providing emotional companionship services by capturing dialects and refining accent granularity. In 2024, with the maturity of multimodal technology, Doubao quickly integrated the Seedream 2.0 model to enhance its text-to-image capabilities.

Doubao’s product strategy is quite similar to that of Douyin, as both are based on “first principles,” continuously optimizing features around the characteristics of new technologies and users’ underlying needs. This not only significantly enhances user experience but also achieves a “snowball effect” through low-cost viral dissemination. By the end of 2025, 36Kr reported that Doubao’s daily active users surpassed 100 million, making it the product with the least promotional expenses to reach this milestone in ByteDance’s history.

Tencent’s Calm Amidst Challenges

Despite Yuanbao’s inability to establish a foothold in the AI industry to date, Tencent has not rushed into laying out new AI businesses indiscriminately. Ma Huateng stated, “We can’t just look at others and casually jump in to seize their territory; we have done that in the past but mostly failed.”

In contrast, during the early days of the mobile internet, Tencent exhibited a strong sense of crisis, continuously entering fields like microblogging, mobile IM, and mobile operating systems. At the end of 2013, during the WE conference, Ma Huateng stated, “Every entrepreneur should have a ‘reset’ mindset in the face of the mobile internet.”

Facing the revolutionary wave brought by AI, Tencent’s response has been relatively calm. On one hand, this is due to the fact that AI technology is still in the exploratory stage and has not yet reached a critical “match point.” On the other hand, it is also because its foundational business is quite stable.

With the rapid development of the mobile internet, smartphones have gradually replaced PCs as the primary computing platform. During this process, social products more suited to mobile internet needs, like microblogging and mobile IM, have risen strongly, continuously diverting QQ’s influence, posing challenges to Tencent’s social relationship chains.

While AI technology holds vast imaginative potential, it has not yet spawned entirely new social products. In this context, Tencent’s social relationship chains remain robust, and the advertising, gaming, and payment commercialization systems extending from its social ecosystem still possess strong competitiveness.

According to financial reports, as of the end of March 2026, the combined monthly active users of WeChat and WeChat reached 1.432 billion, a year-on-year increase of 2%, nearly equivalent to the entire Chinese mobile internet.

In Q1 2026, Tencent’s revenue from its four main business segments—value-added services, marketing services, fintech and enterprise services, and others—was 96.11 billion yuan, 38.171 billion yuan, 59.885 billion yuan, and 2.292 billion yuan, respectively, with year-on-year growth of 4%, 20%, 9%, and 103%.

Overall, in Q1 2026, Tencent’s revenue reached 196.458 billion yuan, a year-on-year increase of 9%; Non-IFRS net profit was 67.905 billion yuan, up 11% year-on-year; and the gross margin was 57%, a year-on-year increase of 1 percentage point.

However, it is quite unusual that despite steadily climbing performance, Tencent’s stock price has been on a downward trend. As of May 15, Tencent’s stock closed at 456.4 HKD per share, down 32.65% from its peak of 677.7 HKD per share at the end of October 2025.

The reason is that the capital market not only focuses on short-term performance but also cares about the long-term growth potential of the company. While Tencent’s performance is impressive based on its existing mature business lines, it faces significant uncertainty about its future as it has not yet outlined a strong growth trajectory in the AI era.

AI Commercialization: Doubao to the Left, Tencent to the Right

Since 2026, as Agents mature, AI applications have entered deeper waters, prompting many tech companies to explore the commercialization of AI products.

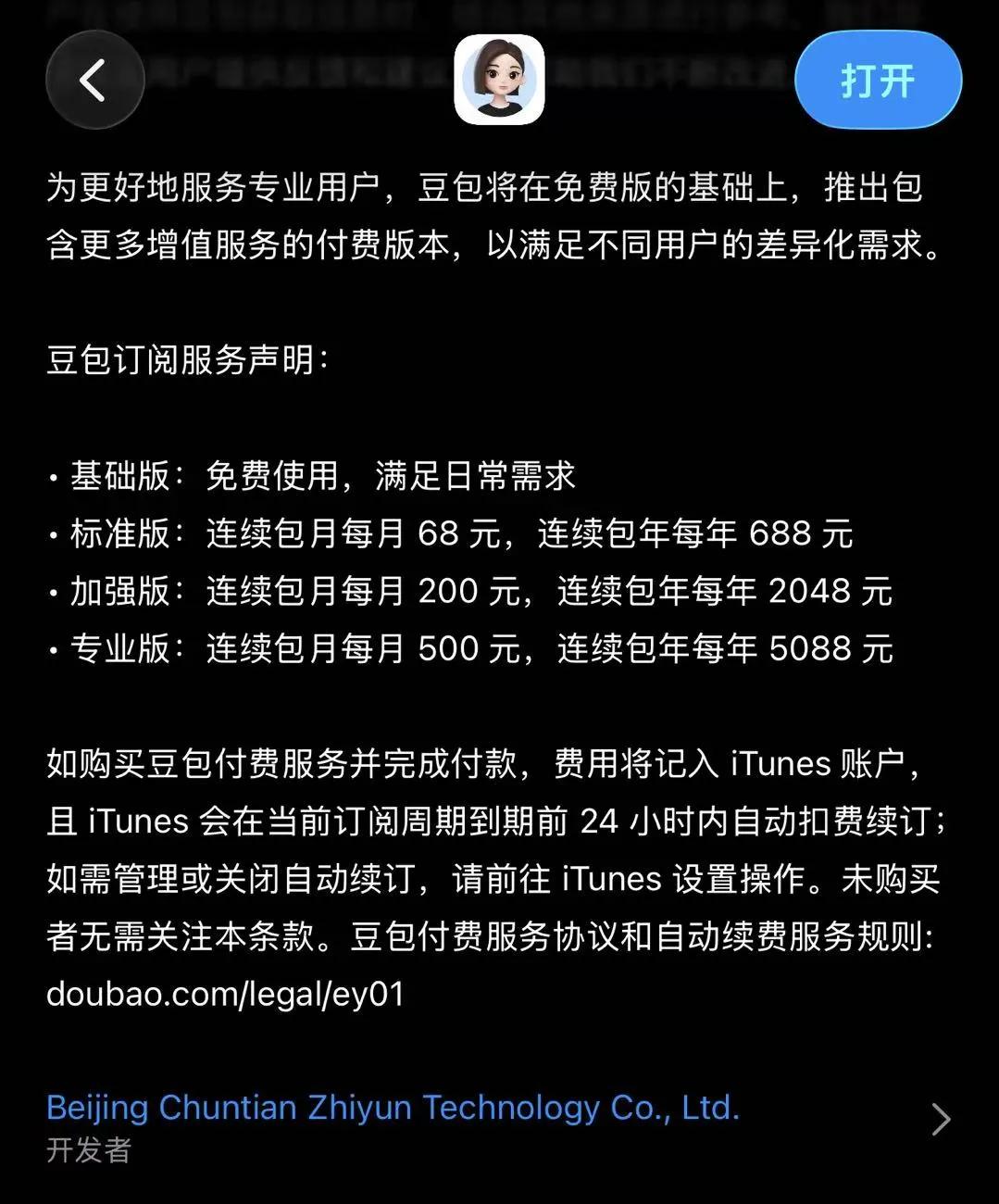

A typical example is Doubao, which announced three “subscription plans” in the App Store in early May, priced at 68 yuan/month for the standard version, 200 yuan/month for the enhanced version, and 500 yuan/month for the professional version, focusing on complex tasks and productivity scenarios including PPT generation, data analysis, and film production.

In fact, Doubao’s approach is not an isolated case; currently, leading AI products like ChatGPT, Claude, and Gemini have also launched multi-tiered subscription systems for consumer users. After paying, users can unlock advanced reasoning models, in-depth research, code generation, and data analysis features that enhance productivity.

However, Tencent does not endorse this commercialization path. During the Q1 2026 earnings call, Liu Chiping stated that in the domestic market, the subscription model for AI products targeting consumer users faces significant challenges, with the penetration rate of paying users currently remaining in single digits, making it difficult to replicate the large-scale subscription growth seen overseas.

In fact, even OpenAI is struggling to achieve a commercial closed loop through subscriptions. Official data shows that as of February 2026, ChatGPT had over 50 million individual subscribers and over 9 million paying enterprise customers.

However, despite having tens of millions of paying users, ChatGPT is mired in losses. Internal financial forecasts at OpenAI indicate that the company expects to lose $14 billion in 2026, with cumulative losses from 2023 to 2028 reaching $44 billion, with profitability anticipated as early as 2029.

Given the difficulties of charging users directly, Tencent has taken a different route—actively developing Agents based on WeChat.

According to The Information, the WeChat Agent is set to launch in Q3 2026, capable of connecting millions of mini-programs within the WeChat platform to meet the needs of billions of WeChat users for ride-hailing, food delivery, online shopping, and more.

In this regard, Ma Huateng stated, “WeChat mini-programs have long adhered to a decentralized approach, with hundreds of thousands of service providers promoting their services through their own channels rather than relying on centralized platform traffic. In the future, WeChat Agent will continue this philosophy, balancing centralized capabilities with decentralized distribution to avoid service providers being ‘short-circuited’ or ‘channelized.’”

Clearly, WeChat Agent may continue Tencent’s core strategy from the mobile internet era, not charging users directly but prioritizing the establishment of an open ecosystem platform. By attracting users and developers through free and open Agent capabilities, Tencent can later achieve commercialization through service commissions, fees, and advertising distribution once the ecosystem matures.

Indeed, WeChat has a vast mini-program ecosystem, with numerous developers and businesses providing services, giving it a natural advantage in developing Agents. However, it is important to note that Agents differ from traditional internet businesses; rapid user growth does not dilute marginal costs but can lead to soaring costs due to surging demand.

For instance, Manus has a single-task operating cost of about $2. As the user base rapidly expands, computing and operational expenses rise simultaneously, making it challenging to achieve a commercial closed loop, ultimately leading to a decision to “sell” to Meta.

Currently, to provide strong support for the large-scale deployment of WeChat Agents, Tencent is actively acquiring computing power. In Q1 2026, Tencent’s R&D investment reached 22.542 billion yuan, a year-on-year increase of 19%; capital expenditures reached 31.936 billion yuan, a year-on-year increase of 16%. During the earnings call, Tencent’s executives revealed, “The demand for our AI-related services is continuously growing, and this year’s capital expenditure in this area will increase compared to last year, especially in the second half of the year.”

If we exclude investments related to new AI businesses, Tencent’s Non-IFRS operating profit growth rate in Q1 2026 would rise from 9% to 17%. In other words, AI-related investments have consumed nearly half of Tencent’s profit growth rate. As WeChat Agents are deployed and massive computing power demands are released, Tencent’s profit margins may further narrow.

Moving forward, the real challenge for Tencent may not be whether WeChat Agents can be successfully launched, but how to establish a sustainable business model amidst the vast user scale and high computing costs. If cash flow cannot be restored, even if WeChat Agents grow to become a second “mini-program,” Tencent will struggle to enter the “first class” of the AI era.

Comments

Discussion is powered by Giscus (GitHub Discussions). Add

repo,repoID,category, andcategoryIDunder[params.comments.giscus]inhugo.tomlusing the values from the Giscus setup tool.